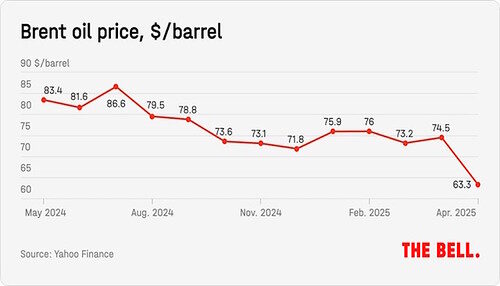

IN SHORT: Brent crude oil fell roughly 6% over the week ending May 9, settling near $101 per barrel on Friday, as President Trump insisted the ceasefire with Iran remained intact despite fresh exchanges of fire between US and Iranian forces in the Strait of Hormuz. The weekly loss was among the largest since 2022 and reflected markets pricing in a higher probability of a diplomatic resolution. But the strait remains effectively closed to commercial traffic, the IEA warned the conflict is removing approximately 1 million barrels per day from global supply, and the Hormuz risk premium in oil has not disappeared.

Oil markets posted their sharpest weekly loss in years on the hope that the Iran-US ceasefire will hold, but the Strait of Hormuz is still closed, South Africa’s July fuel levy cliff is still approaching, and every African oil importer’s 2026 budget is still being written in pencil.

The week’s oil price action reflected a market trying to price two contradictory signals: ongoing military exchanges between the US and Iran that would normally push prices higher, and consistent presidential messaging from Washington that war is not the objective and a deal remains possible.

- Brent crude futures rose 1.2% to settle near $101 per barrel on Friday May 9 as renewed clashes between the US and Iran raised doubts about ceasefire durability. Despite that day’s gain, the contracts posted a weekly loss of approximately 6%, the largest since the post-COVID market normalisation period in 2022. West Texas Intermediate settled marginally higher at $95.42. The week’s range ran from above $109 on Monday to Friday’s close near $101, a $8 swing that reflects acute uncertainty about the conflict’s trajectory.

- The specific incidents driving the price action were severe. The US and Iran exchanged fire on Thursday May 7 in the Strait of Hormuz. Iran launched missiles at the UAE on Friday May 8 for the second time in a week. The US responded by firing on two empty Iranian oil tankers attempting to evade its naval blockade. Trump insisted through each exchange that the ceasefire remained technically in effect, a framing that markets accepted with limited conviction but sufficient to prevent a return to the $114 spike of May 4.

- The International Energy Agency’s warning that the conflict is removing approximately 1 million barrels per day from global supply provides the structural context. The strait has been effectively closed to commercial shipping since late February. The backlog of vessels, cargoes and refined products that needs to clear once the strait reopens means that even a peace deal does not immediately translate into normal supply flows. Analysts at Chevron estimated full normalisation could take weeks after any ceasefire takes hold.

- For Africa the directional shift in Brent from $114 to $101 is meaningful but not transformative. South Africa’s May 6 diesel price increase to R32 per litre was calculated on a Brent average well below $114. The more relevant question for South African consumers and Treasury is whether Brent stays below $100 before July 1, when the fuel levy relief expires and the full R4.10 per litre petrol levy and R3.93 diesel levy reinstate. At $101, that calculation remains extremely tight. At $90, Treasury’s options improve significantly.

- Nigeria is watching from the opposite side of the oil price equation. As Africa’s largest crude exporter, lower Brent prices compress fiscal revenues that the 2026 budget required at approximately $75 per barrel to balance. At $101 the country is still in surplus territory. A sustained fall toward $85-90 would begin to pressure the fiscal arithmetic.

- Angola, which exited OPEC and has been generating extraordinary windfall revenue from the gap between its $61 budget reference price and actual market prices, sees its windfall compress at $101 versus $114. But at $101 Angola is still generating roughly $40 per barrel above budget assumptions, which remains a transformative fiscal tailwind.

- Gold continued its own trajectory, with J.P. Morgan projecting gold toward $5,000 per ounce by Q4 2026 as the geopolitical risk premium persists. Ghana, South Africa, Tanzania, Mali and the DRC all benefit directly from sustained gold prices at the current elevated levels.

TradingEconomics summarised the week’s oil market dynamic: “Traders continue balancing expectations for diplomacy against the risk of further escalation.”

The Bigger Picture: A 6% weekly fall in Brent is the oil market’s closest equivalent to a vote of confidence in diplomacy. It is not confidence in a deal — it is confidence that a deal is more likely than it was. That is a meaningful shift after weeks of near-uninterrupted price increases driven by the effective closure of the world’s most critical oil artery. For Africa’s oil importers, every dollar Brent falls between now and July 1 directly improves the fiscal calculus of the levy relief exit. For Africa’s oil exporters, the week is a reminder that the windfall era has a ceiling. The $101 price is still extraordinary by historical standards. The direction matters as much as the level.

Source: TradingEconomics / CNBC, May 8-9, 2026